Many people choose a Medicare Supplement plan because they want predictable healthcare costs.

Unfortunately, one thing isn’t predictable:

The premium increases.

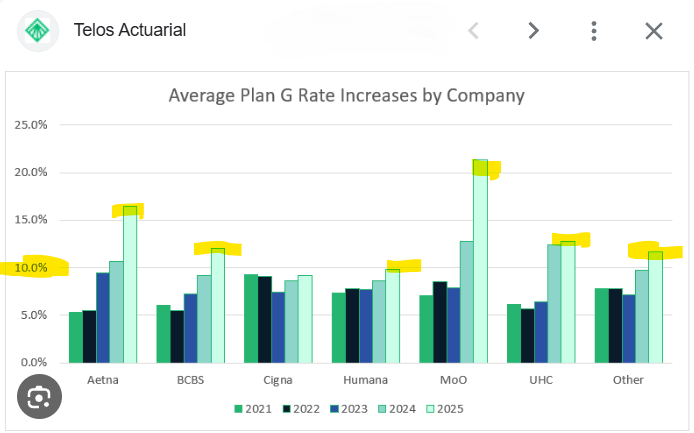

Many Medicare beneficiaries are surprised to discover that Medicare Supplement plans, including popular Plan G options, often increase year after year.

The Real Cost of Waiting

Let’s look at a simple example.

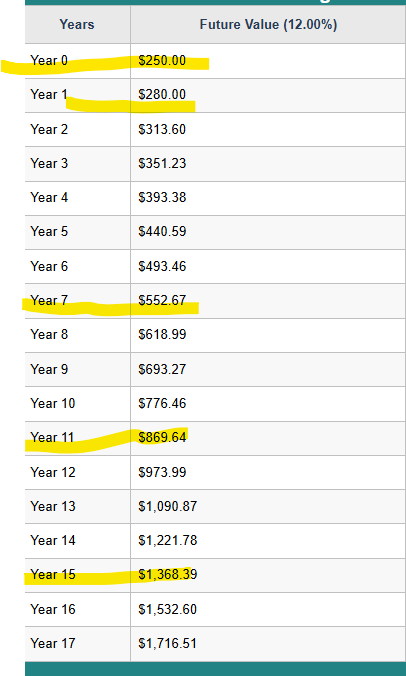

A Medicare Supplement plan that costs $300 per month today may increase substantially over the next decade.

When you add:

- Medicare Supplement premiums

- Part D Prescription Drug Plans

- Dental coverage

- Vision coverage

- Hearing benefits

The total monthly cost can become much higher than many retirees expected.

The Long-Term Impact

An increase of just 8% – 10% annually can significantly affect retirement cash flow over time.

Many retirees eventually find themselves asking:

- Can I still afford these premiums?

- Will my income keep up?

- What happens if I need long-term care?

The concern isn’t just today’s premium.

It’s the cumulative cost over the next 10, 15, or even 20 years.

The Bigger Problem Nobody Talks About

Most people focus on paying Medicare premiums.

Very few focus on how they will pay for:

- Home health assistance

- Assisted living

- Nursing home care

- Custodial care

- Extended recovery services

Medicare was never designed to cover most long-term custodial care expenses.

A Different Approach

At Turn65Medicare.com, we show clients how to evaluate all of their options, not just Medicare coverage.

For many people, saving hundreds of dollars per month can create opportunities to prepare for future elder care expenses while maintaining quality healthcare coverage today.

Bottom Line

The question isn’t just:

“How much does Medicare cost today?”

The better question is:

“How much will it cost me 10 years from now, and what happens if I need care?”